Change State is now part of Recruitics! Learn more

Subscribe to get more insights

Happy Year of the Rabbit! Covering the economy these past few months has felt quite a bit like chasing Alice down the rabbit hole, or staring doubtfully into a crystal ball. The latest jobs report has had people (myself included) asking: what on earth is going on? Interest rates increased significantly in 2022, the stock market had its worst year since 2008, and the looming threat of a recession persists. All together, these factors should make jobs more scarce. It’s difficult even for the experts to agree on next steps, and which are the most likely outcomes in our future. We don’t have all the answers here, but we’re committed to keep tracking trends for you, and highlighting noteworthy findings as the analysis comes out.

WIth that, please find below your Economic Update for February.

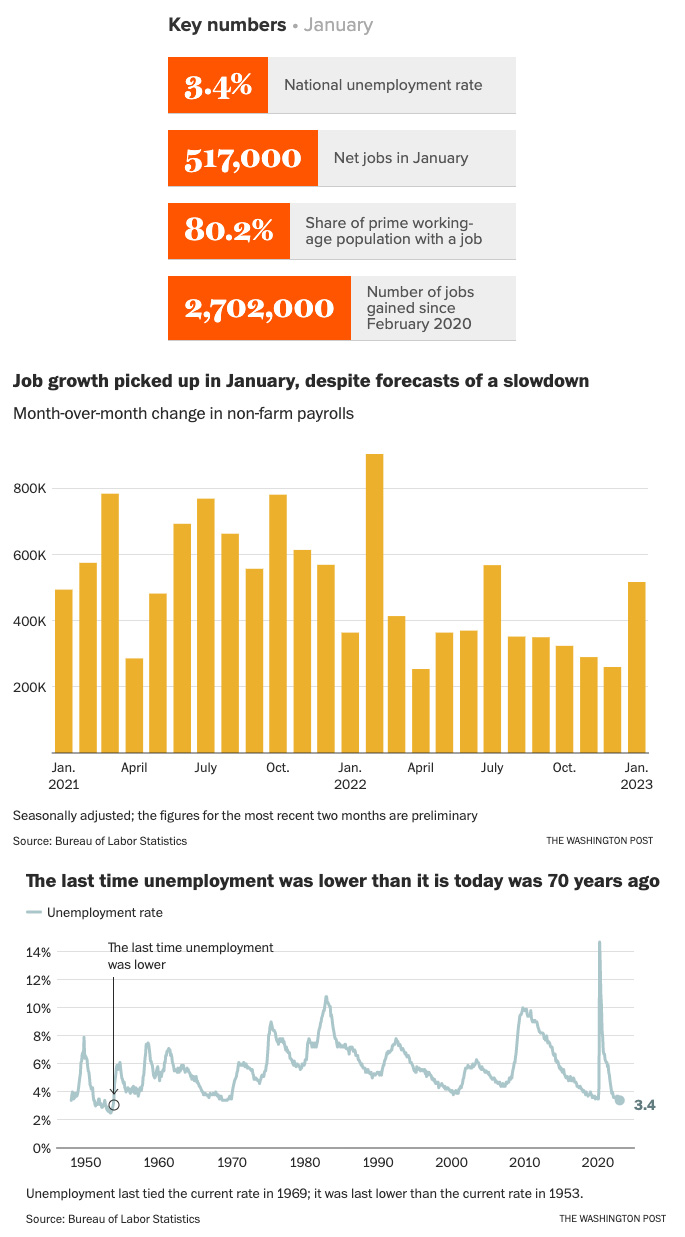

The US economy added an astonishing 517,00 jobs in January and unemployment fell to a new record low: the last time unemployment was lower than it is today was nearly 70 years ago. The unexpected surge seems to have taken everyone by surprise: job growth in January was stronger than foreseen, but then annual 2022 employment revisions were higher as well. The latest report revised total nonfarm payroll upwards for March 2022 by 568K, and December 2022 jobs by 813K. (The more you know: seasonal adjustments are intended to remove the influence of predictable seasonal labor force fluctuations such as the decline between December and January as businesses shed seasonal workers before the start of a new financial year. The intent is to more accurately reveal how employment and unemployment change from month to month.) Job creation in 2022 overall was much stronger than expected, brushing aside notions that the US is very near to recession. Labor force participation rate has continued to trend upwards: to 62.4% in January from 62.3% in December.

Evidence that the labor market may still be heating up? January’s report showed that the length of the average workweek increased (from 34.4 to 34.7 hours) – an indication that companies are not simply hiring more, they are also trying to extract more work from those they have already employed. This suggests that demand for workers continues to be elevated. And while we have all been hearing (and discussing) the never-ending drip of tech industry layoffs, the JOLTS report shows that despite recent news, layoff rates are actually hovering at record lows. What could be the disconnect? Quite possibly our own perception. While the tech industry makes up roughly 4% of overall jobs, when you ask jobseekers where they’d prefer to work, at least 20% say tech. These headlines may seem outsized because of the attention premium we put on companies like Amazon, Meta, and Salesforce.

Another hypothesis is that a phenomenon known as “labor hoarding” is probably exaggerating the strength of the jobs market in January 2023. Labor hoarding refers to the practice of companies holding on to more employees than they need in light of uncertain economic conditions. ZipRecruiter recently surveyed 2,500 people who changed jobs in the last 6 months and 1 in 4 of those say that their previous employer asked them to stay and presented a counteroffer. Employers are eager to hold on to talent until they are confident in the economic outlook. While hoarding is common early in a labor market slowdown, when hoarded labor is eventually released it tends to accelerate job shedding overall.

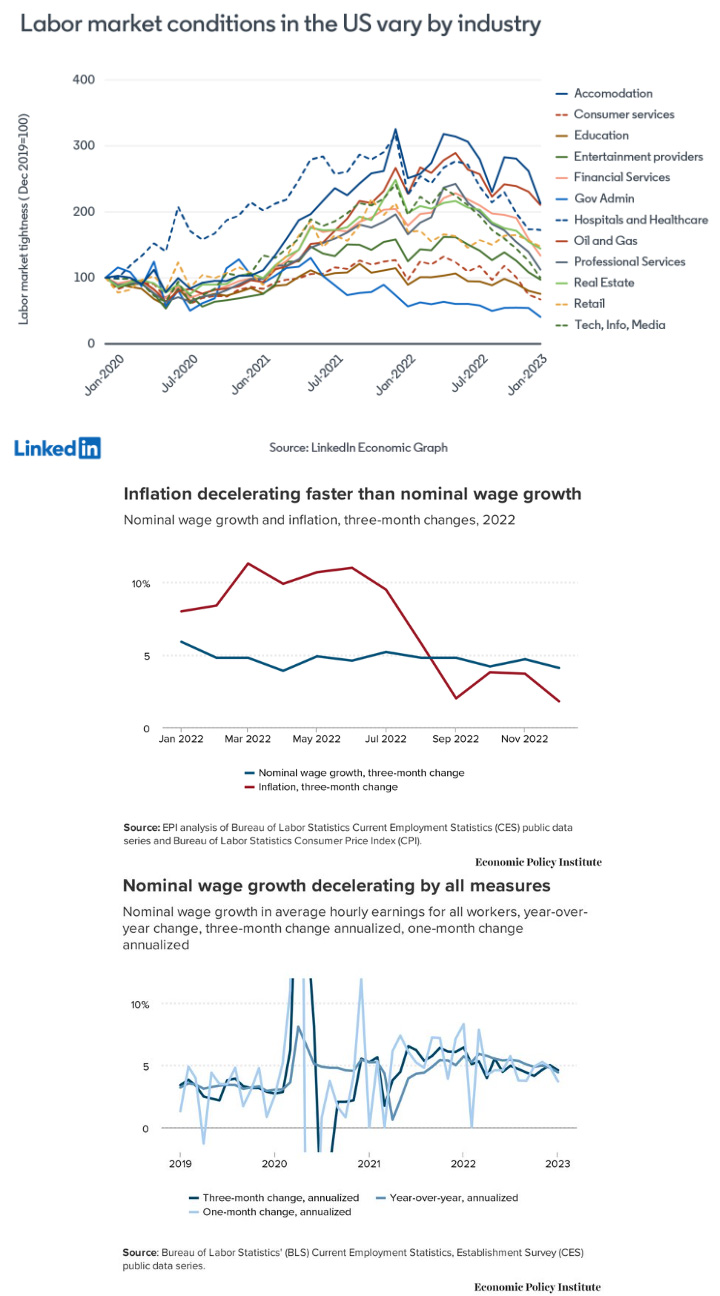

And now for some signs the labor market is actually cooling: LinkedIn’s own measure of labor market tightness – the ratio of open positions to active applicants – has started to decline in recent months.

Temporary employment, a leading indicator of job market strength, has also been declining for several months now. And finally, January’s annualized monthly wage growth was 3.7%, indicating inflation is slowing much faster than wages are rising – a welcome sign if we are to hope for the best case scenario: that the economy can have a soft landing if the Fed plays its cards right.

Evidence that the labor market may still be heating up? January’s report showed that the length of the average workweek increased (from 34.4 to 34.7 hours) – an indication that companies are not simply hiring more, they are also trying to extract more work from those they have already employed. This suggests that demand for workers continues to be elevated. And while we have all been hearing (and discussing) the never-ending drip of tech industry layoffs, the JOLTS report shows that despite recent news, layoff rates are actually hovering at record lows. What could be the disconnect? Quite possibly our own perception. While the tech industry makes up roughly 4% of overall jobs, when you ask jobseekers where they’d prefer to work, at least 20% say tech. These headlines may seem outsized because of the attention premium we put on companies like Amazon, Meta, and Salesforce.

Another hypothesis is that a phenomenon known as “labor hoarding” is probably exaggerating the strength of the jobs market in January 2023. Labor hoarding refers to the practice of companies holding on to more employees than they need in light of uncertain economic conditions. ZipRecruiter recently surveyed 2,500 people who changed jobs in the last 6 months and 1 in 4 of those say that their previous employer asked them to stay and presented a counteroffer. Employers are eager to hold on to talent until they are confident in the economic outlook. While hoarding is common early in a labor market slowdown, when hoarded labor is eventually released it tends to accelerate job shedding overall.

And now for some signs the labor market is actually cooling: LinkedIn’s own measure of labor market tightness – the ratio of open positions to active applicants – has started to decline in recent months.

Temporary employment, a leading indicator of job market strength, has also been declining for several months now. And finally, January’s annualized monthly wage growth was 3.7%, indicating inflation is slowing much faster than wages are rising – a welcome sign if we are to hope for the best case scenario: that the economy can have a soft landing if the Fed plays its cards right.

So what is everyone to make of these puzzling signals? Fed Chair Jerome Powell suggested last week that the central bank believes the labor market is still too hot, and as we are yet in the early stages of disinflation – more rate hikes will almost certainly be necessary, and planned. Other analysts agree, noting that while the Fed has recognized progress on disinflation, January’s report suggests the economy is “more resilient to rate hikes”, reinforcing the need for continued increases.

On the more optimistic side, others are reading notes of positivity in the tea leaves: pointing out that while skepticism on the magnitude of payroll growth is warranted – “almost all the labor market indicators going into this report showed an improvement in labor market conditions.” Janet Yellen, U.S. Treasury Secretary, would agree: “You don’t have a recession when you have 500,000 jobs and the lowest unemployment rate in more than 50 years…What I see is a path in which inflation is declining significantly and the economy is remaining strong.“

“The Fed would be well-served to consider this as a success and think that slowing down the pace of hikes, would allow the job market to bend, but maybe not break…Today presents good evidence of a job market not breaking and evidence of how the economy can adapt and adjust to remain vibrant in the face of major headwinds.”

–Rick Rieder, Chief Investment Officer of Global Fixed Income, BlackRock​

(Sources: Economic Policy Institute, The Washington Post, Job Openings and Labor Turnover Survey, LinkedIn Economic Graph, NPR, Reuters, Yahoo!Finance, ZipRecruiter, The New York Times, Bureau of Labor Statistics, The Conference Board)

What else for February?

(Sources: Economic Policy Institute, Textio, The New York Times, Appcast, Business Insider, Federal Trade Commission, Bloomberg, Accenture)

Software Solutions

Copyright © 2025 Charge State. All rights reserved.

Software Solutions

Copyright © 2025 Charge State. All rights reserved.